Diversification: Stocks & Bonds

In the midst of the current market turbulence, many of our clients are paying more attention to financial markets and their investment portfolios than they otherwise typically might. Rather than allowing headlines to influence our emotions, at PDS Planning we rely upon longer-term data and historical context to put the current environment into perspective and allow us to make more informed decisions.

In light of clients’ rekindled interest and heightened awareness, we thought it would be helpful to review some investing basics through the lens of our time-tested belief that “today’s headlines and tomorrow’s reality are seldom the same.” By sharing our objective outlook, we hope to alleviate some of our clients’ short-term emotional anxiety while achieving better long-term financial results for them.

Diversification

Diversification means investing in a wide variety of assets within a portfolio. The goal of diversification is to limit exposure to any single asset or risk. An easy way to visualize diversification is the typical portfolio pie chart with each slice of the pie representing a different asset class (ex. U.S. Large Cap Stocks, International Stocks, U.S. Bonds). A diversified portfolio has more slices resulting in each slice being smaller, thus spreading out your risk.

The opposite of being diversified, being concentrated, means you have huge slice(s) of your pie in a single asset or asset class. This high risk, high reward approach has the potential to work well if you have a functioning crystal ball but may also have a huge negative impact on your overall portfolio if your big bet concentration does not perform as expected.

Correlation

While we’d all like to invest in assets that only increase in value over time and never lose money, the reality is that asset classes perform differently depending on the current economic and market environment and outlook. Correlation measures how two investments perform relative to one another. A positive correlation means they move in the same direction (i.e. both increase or both decrease). An inverse or negative correlation means when one goes up, the other goes down (and vice versa).

A typical globally diversified portfolio invested in a balanced mix of stocks and bonds owns both positively and negatively correlated assets. While you’d like all of your investments to increase at the same time, you also want to prevent all of your investments from decreasing at the same time. The goal being to achieve the highest portfolio return with the least amount of risk by smoothing out investment portfolio returns over time . Essentially, some assets zig while others zag, resulting in a less bumpy ride along the way.

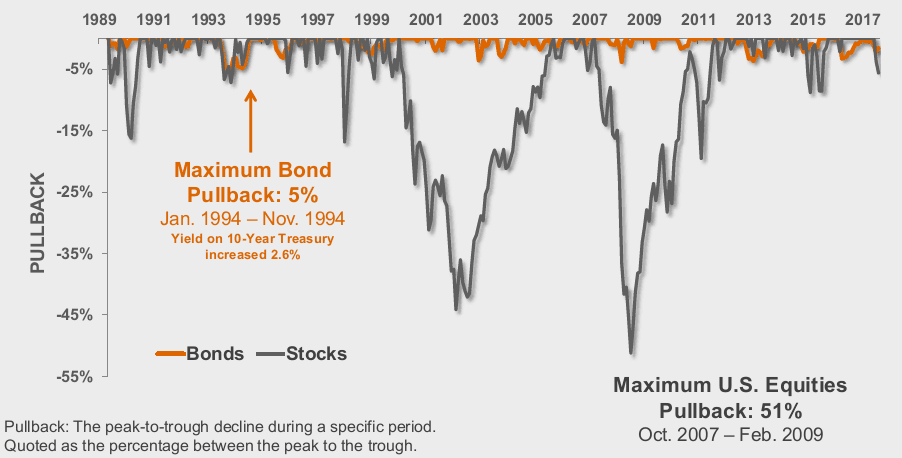

Drawdowns

At an overly generalized and basic level, many people consider portfolio risk to be the mix of stocks versus bonds in their allocation with stocks being considered “risky” and bonds being considered “safe”. The reason many investors include a healthy dose of bonds in their diversified portfolio is to preserve capital during inevitable market pullbacks. As seen in the chart below, over the last 30 years, the maximum drawdown in stocks (-51%) dwarfs the maximum drawdown in bonds (-5%). Bonds provide diversification benefits, in large part, due to their ability to provide downside protection.

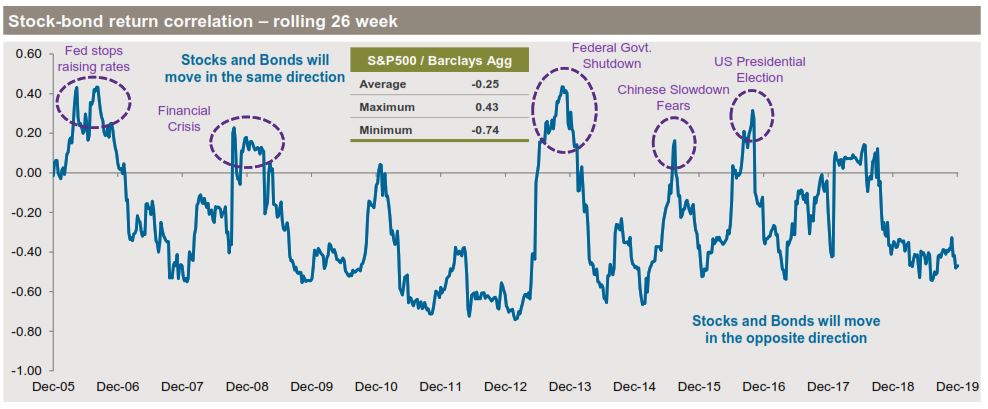

Market Stress

However, these diversification benefits sometimes temporarily break down under periods of market stress and volatility such as our current uncertain environment. With a primary benefit of bonds being the preservation of capital, bonds’ typical negative or inverse correlation to stocks means that, under normal circumstances, when stocks decrease in value, bonds increase in value. In the chart below, you’ll see this negative correlation tends to hold true with a negative/inverse average since 2005; however, there have been a number of periods where bonds and stocks have moved in the same direction (positive correlation) as shown in the purple circles. While these periods of stocks and bonds moving in the same direction (and almost always both losing value at the same time) are somewhat regular, historically they have only been temporary. Still, it may be shocking to look at your portfolio and see all of your investment holdings declining in value (aka. all zigs, no zags). Though it may feel like “this time it’s different”, the below chart is yet another reminder that this too shall pass and the future is always the same.

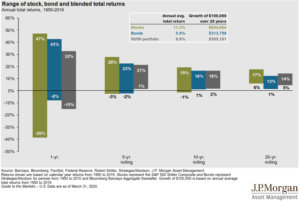

Time, Diversification, & the Volatility of Returns

Over shorter periods of time, investment returns and volatility can vary widely; however, long-term investors are rewarded for their time in the market, not for trying to time the market. Maintaining a diversified allocation that is consistent with your long-term goals, combined with periodic rebalancing, has consistently resulted in beneficial long-term financial outcomes. We remind clients to keep their next 7-12 years of anticipated cash distribution needs in stable assets such as cash, CDs, and short-term bonds.

PDS Planning continues to be available to both our existing clients and prospective clients who can benefit from the financial planning and investment management services we provide. Please contact us if you have any questions or would like to discuss ways we may be able to assist you in providing clarity during these uncertain times.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment, strategy, or product or any non-investment related content, made reference to directly or indirectly in this newsletter, will be suitable for your individual situation, or prove successful. This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Consultation with a qualified investment advisor is recommended prior to executing any investment strategy. No portion of this publication should be construed as legal or accounting advice. If you are a client of PDS Planning, please remember to contact PDS Planning, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives. All rights reserved.