By Drew Potosky, CFP®,

Posted: 7/16/2024

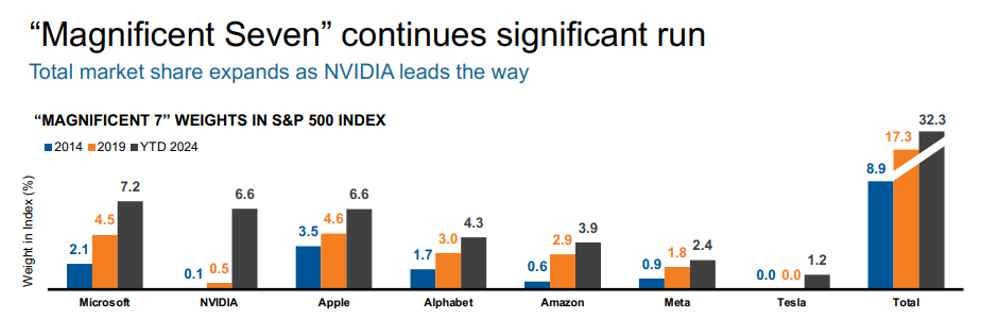

A lot has already been said about the Mag7 stocks and the very prominent role they play in the S&P 500. They account for over 32% of the entire index and, with AI still a major theme, may continue to grow.

Are we getting shades of the 2000 tech bubble? Is that what’s coming next? Stephanie Aliaga, Global Market Strategist with JPMorgan, doesn’t think so.

- “Risk appetite. During the dotcom bubble, rampant speculation surrounded young companies flaunting internet excitement before profitability. In contrast, today’s AI beneficiaries are already very profitable companies that make their money selling key infrastructure and resources to the rapidly growing market of AI adopters. Additionally, interest rates are high, IPOs have slowed to a trickle and global VC investments have fallen from their peak in 2021[1]. While bullish sentiment has surely provided a boost[2], the impact of earnings upgrades is likely more significant—the Mag 7 posted a remarkable +50% y/y earnings growth in 1Q24[3].

- Fundamentals. The Mag 7 account for a sizable 33% of market cap, but they also account for 39% of R&D spending, 23% of free cash flow and 16% of capex (see chart). The strongest are getting stronger, but they’re fueled on veggies and complex carbs, not short-term stimulants.

- Shareholder return. The recent boost in shareholder return can also be attributed to tech strength. Certain mega-cap tech companies have announced substantial share buyback programs or first-ever dividend payouts this year. These announcements have contributed to a 6% increase in S&P 500 shareholder payout in 1Q24, and the S&P return-on-common-equity stands at a solid 18.5%.”

We’re not saying, throw caution to the wind. But some of the data behind the points above do support the idea it may not be the doom and gloom headlines try to portray. However, there are still reasons for pause, especially when we think about tech and the AI rally. “If demand cools off unexpectedly, perhaps because the economy deteriorates, geopolitics, or capacity constraints become a binding factor, such projections could be overly optimistic.”

We agree with what Aliaga says in closing, “The alarm bells may not be ringing like the dotcom bubble. Concentration today appears to showcase corporate resiliency and companies that are at the forefront of growth, but questions abound whether recent performance can be sustained. As such, investors can still enhance diversification by exploring overlooked areas of the market, within and outside of the AI value chain, that have strong fundamentals.” PDS remains diligent in making sure client portfolios remain diversified with global stocks, bonds, and real estate and continue to keep a close eye on the rapidly changing markets.

IMPORTANT DISCLOSURE INFORMATION: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by PDS Planning, Inc. [“PDS”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from PDS. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. PDS is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the PDS’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.pdsplanning.com. Please Note: PDS does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to PDS’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a PDS client, please contact PDS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.