Before I talk about oil prices and inflation scenarios following recent military conflict involving Iran and disruptions to the Strait of Hormuz, a critical chokepoint for global oil supply, I want to focus on some of the market positives.

After a lousy March, the S&P 500 recovered quickly and is up over 8% year-to-date. International developed and emerging market indices have grown 11% and 9% respectively, and US small caps are up over 10%, too. A diversified 60/40 portfolio is up about 8% as well, showing how markets have remained resilient in the face of geopolitical volatility, higher oil and gas prices, and rising inflation.

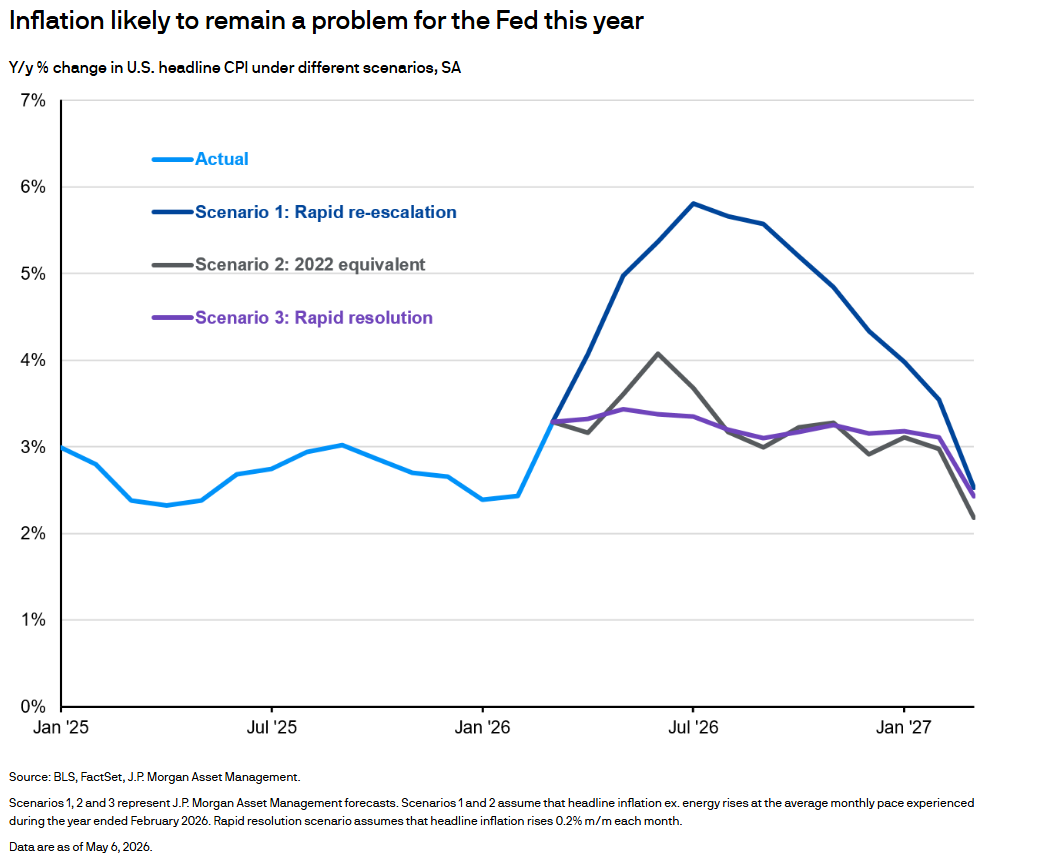

Jordan Jackson and Brandon Hall with JP Morgan tried to answer the question of, “How Inflationary is the oil price spike?” earlier this month. The different scenarios they outlined can be summarized as the good, the ehh, and the ugly and each scenario depends on the length of the conflict in Iran and, more specifically, the Strait of Hormuz.

Scenario 3: Rapid Resolution – Inflation near peak and declines gradually

The Good. “If diplomacy moves faster than expected and oil prices normalize gradually, headline CPI could revert to the average monthly pace seen in the year ending February 2026. Even in this benign scenario, inflation would still remain above 3.0% through February 2027.”

Scenario 2: The 2022 Playbook – Inflation peaks at 4% but declines quickly

The ehh. In 2022, Russia invaded Ukraine and oil prices spiked through the first half of they year, pushing inflation higher due to higher energy prices. If the current state of the conflict persists, investors can expect similarities. It’s worth noting in 2022, we were dealing with the economy opening back up post-Covid, supply chain problems, and inflation already running very hot. While 2022 was a bad year for markets and inflation, “Today’s starting point is much lower, and with demand expected to weaken modestly and disinflationary forces still intact, peak inflation this year should fall well short of 2022’s high.”

Scenario 1: Re-escalation – Inflation peaks over 5% and remains elevated

The Ugly. The US and Iran re-escalate, the Strait remains impassable and even more dangerous, and more damage is caused to the broader oil and energy infrastructure. A week ago, the final tanker from the Strait of Hormuz made it to California before the closure, so a re-escalation will further shock markets and push oil and gas prices higher.

Each scenario carries different market implications, but at PDS Planning we’re prepared for any of them. For clients holding cash, today’s environment still offers attractive options. Money markets near 3.5% and CDs around 4% mean your cash is working while waiting for the right opportunities. We’re also actively monitoring portfolios for rebalancing needs as markets shift and watching for tax-loss harvesting opportunities as volatility creates them. Whatever the conflict resolution looks like, we’ll be ready to act, and we’re always just a conversation away if you have questions.

IMPORTANT DISCLOSURE INFORMATION: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by PDS Planning, Inc. [“PDS”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from PDS. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. PDS is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the PDS’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.pdsplanning.com. Please Note: PDS does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to PDS’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a PDS client, please contact PDS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.