Economic and Investment News Bits

- “Job growth last month shifted to higher-paying positions in a sign of a broadening labor market recovery. Professional and business services, construction and health care led the solid 223,000 job gains reported by the Labor Department last Friday. The trend reflects a widening recovery that includes a pickup in full-time positions. While retail, leisure, and hospitality lagged, they have been sources of growth through most of the employment upswing since 2010,” (Source: Ivy Asset Mgmt).

- The 11/26/2012 issue of Time magazine ran an article titled “Why Stocks are Dead”, which documented the gloomy equity forecast of money manager Bill Gross. From that date to the close of trading on May 8, 2015 (about 2 ½ years) the S&P 500 Index has gained +58.4%. (Source: Time)

- For all of the doom-and-gloom predictions, the most recent quarterly corporate earnings reports have come in nearly 6% better than expected, the biggest out-performance since 2012. Sifting through the forest for the trees, however, it was the mega-caps that posted most of the gains. About three-quarters of the largest 50 companies beat expectations, but only about half of small and mid-sized companies. (Source: Federated Investors)

- Recent research has uncovered the factors that influence migration patterns of college graduates, ages 22-35, among 260 metro areas, large and small. The most important factors were, in descending order: 1) a high density of people with a college degree, 2) a low unemployment rate, and 3) the ability to get around without a car. Top major metro areas were Washington, San Francisco, Boston, San Jose, and New York. Columbus ranked number 12, ahead of Hartford, Chicago, and Pittsburgh.

- Stratfor Global Intelligence predicts the agriculture industry will “continue to adapt, improvise, consolidate and automate in order to overcome challenges of a rising population and an increased scarcity of resources. Robotics, smart technology and drones are among the things that will be increasingly incorporated into the industry as producers cope with increased global demand, declining resources and rising labor costs. Driverless tractors, drones that monitor soil quality, automated irrigation and even robotic bees to pollinate crops are all tools farmers will have at their disposal.”

Thought for the week

“Don’t cry because it’s over. Smile because it happened.”

Dr. Seuss, American writer (1904-1991)

Investment Idea of the Week

There is a huge change coming, says economist Louis-Vincent Gave. China is pressuring the International Monetary Fund to add the Chinese renminbi (RMB) to the basket of four currencies (US$, euro, UK pound sterling, Japanese yen) that make up the majority of international trade and foreign exchange reserves. “They will probably get their wish at the November 2015 IMF meeting. This will let other central banks hold RMB, which they will do because it has a much higher yield than the other currencies. The result will be the lifting of Chinese capital controls and a sharp increase in China’s weighting in world equity indexes, forcing all indexes to buy Chinese stocks. Asia is in a broad bull market that will continue. Europe is now in the sweet spot – a must-seize opportunity.”

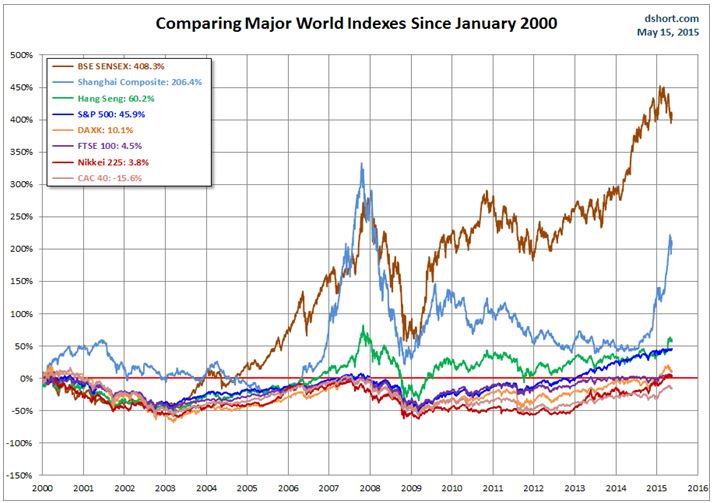

Graph of the Week (CLICK TO ENLARGE)

Here is a look at how the main equity markets have performed in the 21st century. India’s SENSEX index has topped the charts with a return of over 400%, while Shanghai follows in second at just over 200%. Hong Kong has returned about 60% since 2000, and the U.S. about 46%. Europe has lagged with Germany only up 10%, the U.K. 5%, and France -15%.

This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. All rights reserved.