Economic and Investment News Bits

- Ahead of Greek national elections this month, a likely opposition victory could result in default on outstanding government debt and the country’s exit from the euro area. Speculation has it that Germany would accept Greece’s departure from the currency bloc. (Source: Bloomberg)

- “Volatility, which retuned in a big way in December, is likely to continue in 2015. Slowing global economic growth, more activist central bank policies, and the collapse in commodities are three visible causes,” (Source: Bank of America).

- “The long-term technical chart of West Texas Intermediate (WTI) crude oil shows a near-perpendicular drop in price. If it were a stock, it would suggest that a corporate bankruptcy was ahead. The drop has persisted too long to represent a simple supply/demand adjustment. With crude oil now trading more than 40% below its 200-day moving average, it should be able to find its footing and its real supply/demand balance early in 2015. And keep in mind that energy-related employment is just 0.6% of total employment” (Source: Dudack Research).

- No one talks about the deficit anymore. The S. federal deficit is on track to be 2.5% of GDP for 2014, matching its historical average, versus 10.1% in 2009. The improvement has been due to federal receipts growing by over $1 trillion since 2010, with expenses basically flat. Still, federal debt as a percentage of GDP is 73% in 2014 versus 35% in 2007. (Source: Treasury Department)

- “There are five core lessons I have learned over the course of my investing career that form the foundation of my annual surprise lists: 1) How wrong conventional wisdom can consistently be. 2) That uncertainty will persist. 3) To expect the unexpected. 4) That the occurrences of “black-swan” (unprecedented and unpredictable) events are growing in frequency. 5) With rapidly-changing conditions, investors can’t change the direction of the wind, but we can adjust our sails (and our portfolios) in an attempt to reach our destination of good investment returns,” (Source: John Mauldin)

- The 2014 mean return for 36 selected stocks of companies based in Central Ohio was 2.2%. Glimcher Realty was the top gainer, up 46%. (Source: Yahoo Finance, The Columbus Dispatch)

Thought for the week

“It is unthinkable that any child should go hungry in the country that grows more food than any other.”

Sela Ward, American actress (b. 1956)

Expecting Higher Interest Rates, Version 5

It seems the Federal Reserve Board has confounded the experts for more than five years, as they have managed to create a slow-growth economy that has low inflation and still-problematic employment numbers. This is all despite the Fed’s liabilities ballooning from less than $1 trillion in 2008 to almost $4.5 trillion in 2014 as a result of its Q E government bond-buying spree. Consensus now seems to be that the Fed will start raising short-term (Fed Fund) rates in the third quarter of 2015. It was widely believed that QE would cause higher inflation rates, which would force the Fed act much sooner than it has. The truth is that most long-term bonds are already at or near record-high prices. Yes, investors could still push prices higher, but once the bubble bursts, it might well be “Watch out, below!”

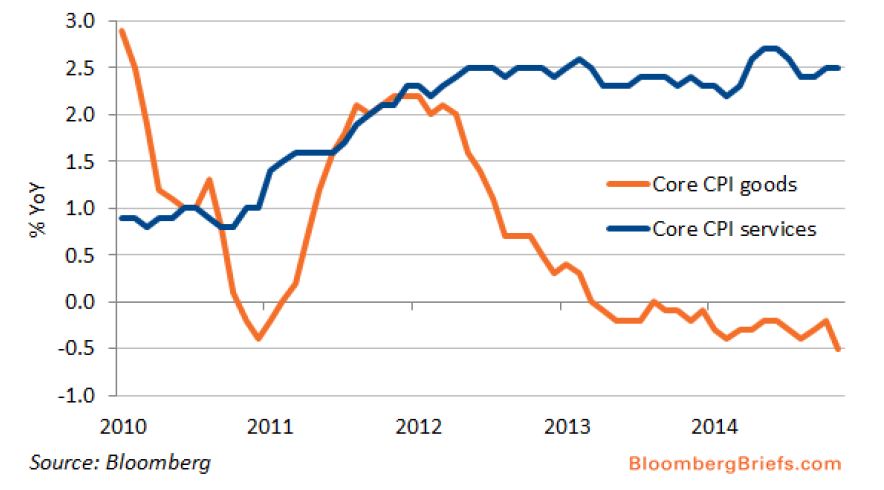

Graph of the Week (CLICK TO ENLARGE)

Core inflation appears more benign than what’s brewing beneath the surface. Monetary policy makers grapple with still-too-low inflation as an increase in fed funds’ rate approaches. Core inflation is running below the Fed’s 2 percent target. Yet its causes are unrelated to weak fundamental demand. Core goods inflation has actually become negative, due to a stronger dollar weighing on import prices and to falling energy prices. Meanwhile, service sector inflation is already running hot, spurred by rental pressures that are unlikely to vanish given a low rental vacancy rate. Other service categories are set to accelerate as the labor market continues to mend — their largest input cost tends to be wages.

This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. All rights reserved.