Economic and Investment News Bits

- Regarding the ongoing drop in oil prices, HardAssetInvestor says “Energy traders are now targeting the 2008/2009 crash low as a potential bottom, which are $32.40 for West Texas Intermediate (WTI) and $36.20 for Brent Crude. Of course, during a precipitous free-fall like the current one, all the technical indicators go out the window. Ultimately, we will know where the oil bottom is only in hindsight.”

- Despite a gain of more than 14% in 2014, Chinese equities continue to be the brunt of much criticism by market observers. Stocks there have rallied strongly since last summer despite the country’s slowdown. China’s market capitalization has surpassed that of the other BRIC countries combined. There is still risk there, but it’s still the fastest-growing, large economy in the world.

- U.S. Global Investors notes that “For the first time ever, the German 5-year and 10-year government bond yields have fallen below zero, indicating deflation in the eurozone. This means that German bondholders are effectively paying the government to hold on to its debt. As a result, international investors are looking elsewhere – gold, for instance, or the U.S. municipal bond market.”

- In early July, 2010, self-proclaimed market guru Robert Prechter forecasted that the Dow Jones Industrial average would fall below 1,000 within 6 years. After almost 4 ½ years, the Dow closed 17,737 last Friday.

- Cattle ranchers are starting to use advanced DNA technology in order to asses a bull’s genetic value. Neogen Corp developed the tests (currently $100 per animal), and the analysis from them helps breeders identify prize animals that will yield a larger volume, returning much higher prices from processors. Other companies are starting to invest in this technology, including Cargil, Zoetis, and BeefTek. (Source: Wall Street Journal)

- It’s not just football. University of Oregon – founded in 1876, endowment of $552 million, ranking #106 among national universities, 20,797 undergraduates, 73.90% acceptance rate for incoming freshmen, $9,918 annual tuition. Ohio State – founded in 1870, endowment of $3.1 billion, ranking #54 among national universities, 44,201 undergraduates, 55.50% acceptance rate for incoming freshmen, $10,037 annual tuition.

Thought for the Week

“Don’t look back. Something might be gaining on you.”

Satchel Paige, American athlete (1906-1982)

Wealth Idea for the Week

Despite some recent volatility in the stock markets, investments with “happy looking” trailing returns have caused some investors to inadvertently tilt their portfolios toward higher-risk investments. It is important to look at the risk profile of a portfolio. Look at returns for holdings in 2008, for example, or at the up-market or down-market capture ratios for funds. Focusing solely on returns, especially in 2014, could lead to over-weighting large cap domestic stocks. When that sector becomes overheated (some believe it already is), portfolio returns could be in for a nasty surprise. It is important to have some holdings that are boring, that are designed to provide balance. Being careful in 2014 most likely meant low single-digit returns. The diversified Morningstar World Allocation Index returned just over 1% in 2014. But before you change the risk profile of your portfolio, ask yourself if you can handle a loss of 35-50% from the stock portion of your investments. That is what happened to stocks in 2008, and it was not pretty for most investors.

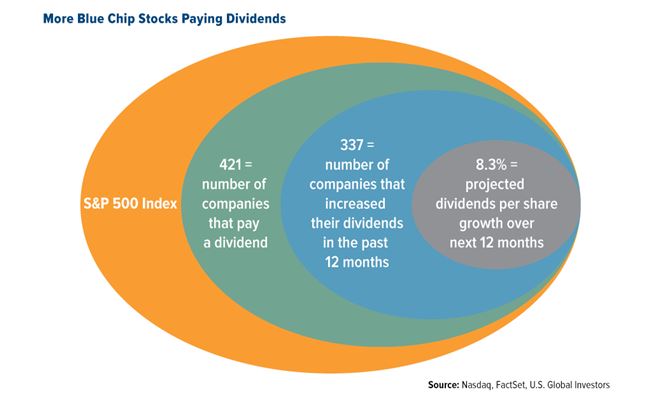

Graph of the Week (CLICK TO ENLARGE)

Nearly 85% of companies in the S&P 500 currently pay a dividend, with dividends per share having grown 11.3% in the past 12 months. What’s more, FacSet analysts expect dividends per share to increase over 8% in the next 12 months, with the financial and consumer discretionary sectors to report double-digit dividend growth.

This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. All rights reserved.