Economic and Investment News Bits

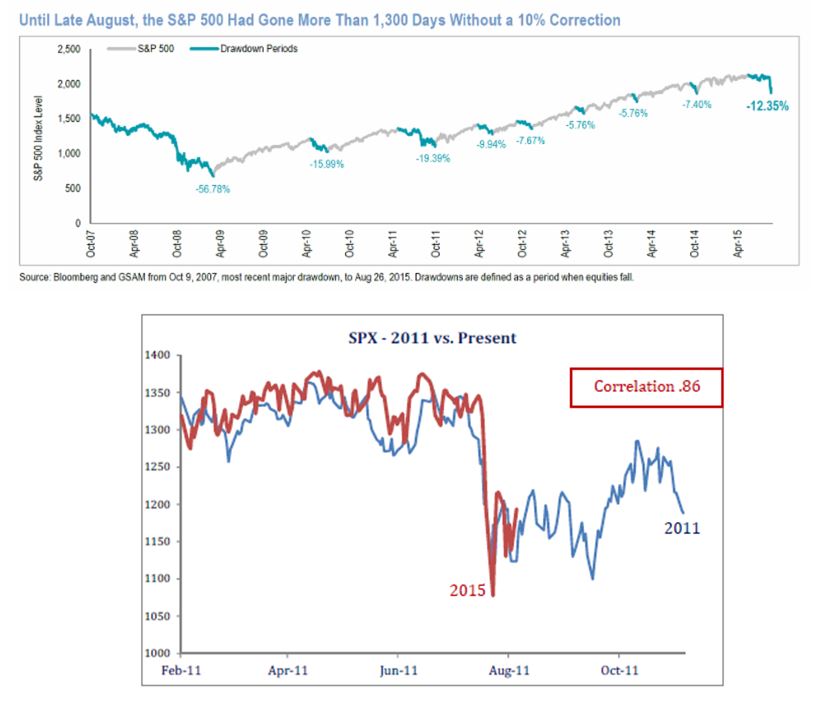

- In last month’s Viewpoints, we suggested that “the current market weakness” might portend a correction. It seems we may have been onto something, since the S&P 500 Index was down more than 12% from its high on August 24 (currently it is down 8%). A true correction would drop the markets 10-15%. A number of things are causing instability right now, including the pending Fed decision on interest rates, lower oil prices, and potential slower growth in China.

- Most economists expect China’s GDP to come in just under 7%, which is the Chinese government’s target, and far better than the doomsday predictions from the broadcast media. “All governments intervene during periods of pain, China is no exception, working to steadily pump growth during a multi-year transition for the economy” says Brian Jackson of HIS Global Insight.

- “Some investors might worry that falling energy prices are creating havoc for the S&P 500 Index,” notes Frank Holmes. “Currently energy is only 7% of the index, and its position is dropping. Energy has a minimal impact on the overall index. It often takes a few quarters before the benefits of lower oil prices are realized with non-energy companies such as the airline industry. The longer fuel prices stay low, the more likely it is that airlines will perform beyond expectations.”

- Ned Davis research noted key reasons why there has been very little upward pressure on wages: demographic shifts (boomers retiring), slow productivity growth, faster job growth in low-wage industries, more part-time workers, more temporary workers, less unionization, and increased globalization.

- “If Washington can reach a compromise on the current international corporate tax system, there could be $200 billion in extra revenue for the federal government and $1.9 trillion in available cash for corporations. The government could fund much of the desperately-needed infrastructure spending, while companies could increase mergers and acquisitions and add jobs.” (Source: Philip Orlando).

- More opportunity for economic growth? The average unemployment rate for the 19-country Eurozone was 10.9% on July 31, a 3 ½ year low. The unemployment rate in the U.S. was 5.1% on August 31, a 7-year low. Europe is about five years behind the U.S. in terms of job growth.

Thought for the week

“We don’t stop playing because we grow old. We grow old because we stop playing.”

George Bernard Shaw, Irish author (1856-1950)

Perspective on the Current Market Volatility

As we have noted previously, market corrections are common, with an average intra-year decline of more than 14% since 1980. However it has been nearly four years since the last correction in August, 2011.

The above graph (Click to Enlarge) from Strategas Research Partners indicates how similar this August’s decline was to the market decline of August, 2011. During that period, U.S. stocks dropped 19% before finishing the year with a gain. In 1998, events similar to now were happening, including dropping oil prices, lower emerging market stocks, and financial issues in Asia. Then, stocks dropped 18% before finishing the year in positive territory. Investors have been lulled into a false sense of market stability these past four years. When we add in this week’s Fed meeting, there may be even more volatility in the short term. Unlike 2011, bonds are not having a good year. However, as conditions smooth, and with a recession unlikely, there might be an opportunity to put cash to work.

This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. All rights reserved.