Welcome to our November 2023 Viewpoints, a monthly bulletin from PDS Planning to our valued clients and friends. Our goal with each issue of Viewpoints is to provide you with a wide variety of perspectives on life and wealth. Feel free to share with others.

Finishing Strong, and Top Heavy

After a tough stretch from the end of July through the end of October, most of the 3rd quarter, the stock market (S&P 500) has bounced back in a big way since then. It took 65 market days to lose about -10.50%, then only 18 trading days to make nearly all of the loss back. While we love to see more green than red, it also provides a good reminder on the importance of staying invested!

We’ve talked about the performance of the top stocks in the S&P 500 index providing most of the year to date return, the magnificent 7 as they’ve been dubbed. These large stocks have continued pushing higher while the rest of the index has all but maintained value. The market breadth has been narrow. And as it remains narrow, the weighting of the top 10 stocks continues to grow. As of close of market 11/21, the top 10 stocks make up 33.3% of the index by market capitalization. This has been a benefit year to date since the top 10 have been performing the best, but it is something to continue to be mindful of on the grounds of diversification.

Tag, You’re It

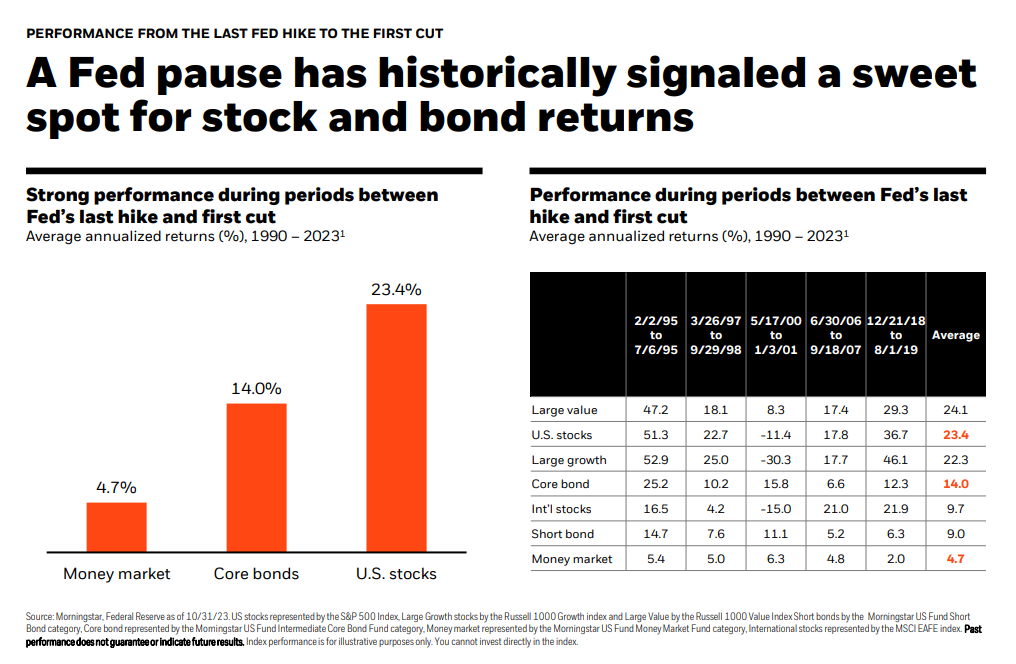

After storming higher quicker than ever before, interest rates appear to be settled at current rates after Fed minutes have pointed toward a pause on more rate hikes. Looking back at the last 5 periods of rate pauses (the time between the last hike and first cut), rates appear to tag markets in – and appear to have done so this year already – as the average annual return for stocks and bonds has been 23% and 14% during those time periods, respectively.

*pssht* This is your Captain Speaking

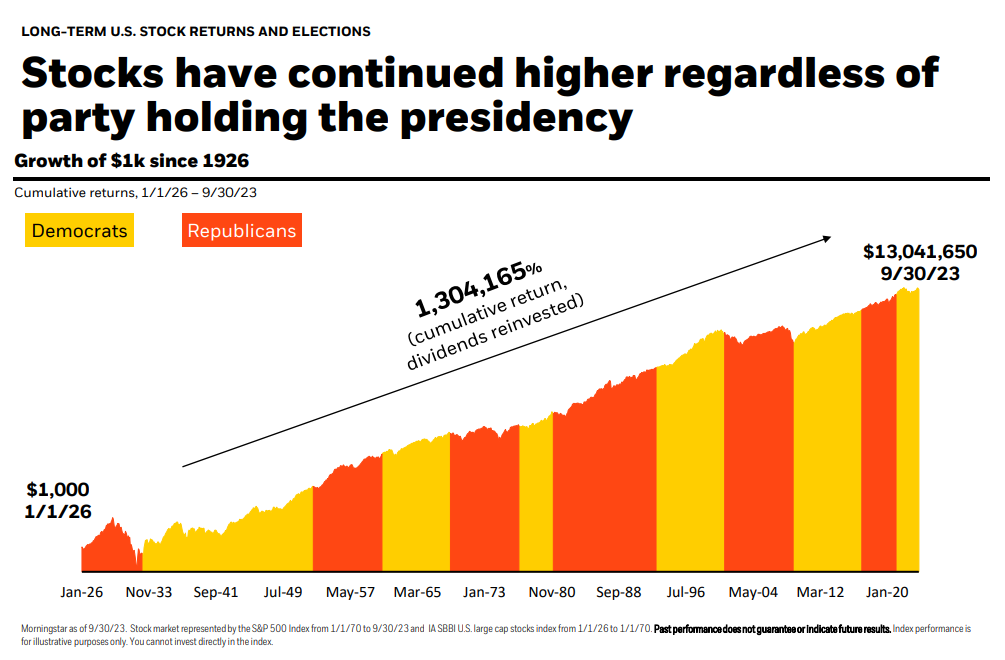

2024 is another Presidential election year, so politics will undoubtedly be put up against economic and stock market performance. Regardless of which way you may lean, history shows us party doesn’t matter to the markets. Long-term investors have benefited from remaining invested regardless of who’s at the helm. There will almost certainly be an increase in market volatility with an unknown as important as the President creeps closer, but like we looked at above, change can happen quickly!

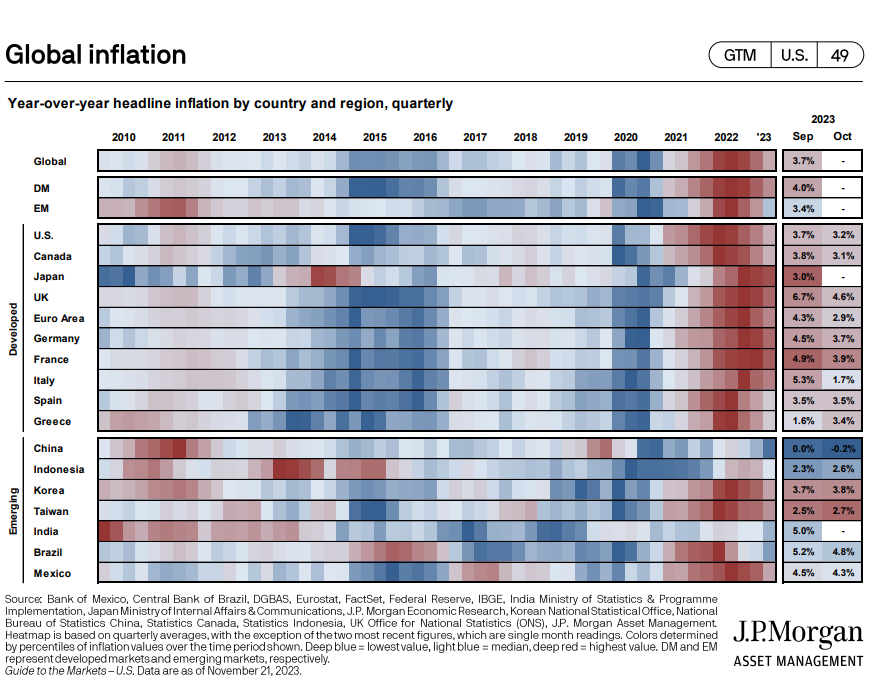

Inflation is Cooling Across the World

After nearly two years of rising inflation, countries around the world – in both developed and emerging markets – are seeing it cool down. Where red is high inflation and blue is lower, the chart still makes it look pretty messy. But the overall sentiment is inflation has been getting better, more manageable. Manageable for central banks and the Fed, and more manageable for the consumer.

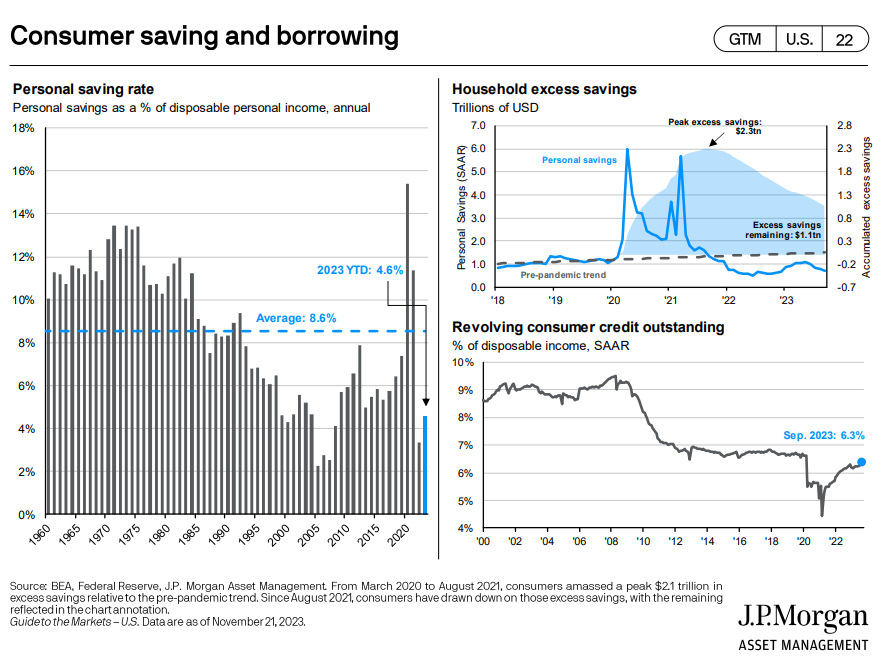

In the US, savings rates are down compared to pre-covid years (left chart), but households still have excess savings (top right chart) to help weather the higher prices for their household expenses.

IMPORTANT DISCLOSURE INFORMATION: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by PDS Planning, Inc. [“PDS”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from PDS. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. PDS is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the PDS’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.pdsplanning.com. Please Note: PDS does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to PDS’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a PDS client, please contact PDS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.