December 2020 Financial Markets Summary

November was another strong month for the markets with positive news of vaccine results. Small cap stocks bounced by nearly 20% and energy, which has lagged for most of the year, jumped up 30%. However, recent flare-ups across the country suggest that the virus has yet to be contained and “will likely continue to impact near-term growth,” according to U.S. economist Jared Franz. “All growth forecasts depend on the trajectory of the vaccines.” Schwab’s Liz Ann Sonders also added that “if vaccines represent the light at the end of the tunnel: the virus means we are still in a fairly dark part of the tunnel.”

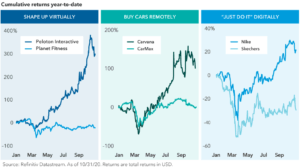

The COVID-19 pandemic has caused personal and economic impact that could last for years. A look beneath the surface reveals that major sectors have moved in sharply different directions, reflecting the disparity between companies that have benefitted from the COVID-19 pandemic and those that have been decimated by it. For restaurants, hotels, retailers, airlines and small businesses, it has literally been the worst of times. At the opposite end of the spectrum, the stay-at-home era has been a boon for e-commerce, cloud computing, video streaming, digital payment processors and home improvement stores.

According to Capital Group, “the digital gap that existed long before the coronavirus outbreak has suddenly become a digital Grand Canyon. Black Friday, the traditional start of the holiday shopping season, offered a clear illustration of the divide. About half as many consumers visited stores on Black Friday 2020 as did a year earlier, according to the Wall Street Journal. Meanwhile, online holiday shopping was expected to rise about 22% to $202 billion, according to the National Retail Federation.”

Companies with fast and efficient online business models are soaring above the competition, disrupting the status quo and displacing the old-economy stalwarts. Capital Group’s Chris Buchbinder suggested that “we were already headed in this direction when COVID came along and it gave it a huge shove forward.”

We are not necessarily out of the woods now that vaccines are just around the corner. Markets will continue to experience volatility and there will be long-term winners and losers, but we hope you and your family have a safe holiday season!

| Asset Index Category |

Category |

Category |

5-Year |

10-Year |

|

2020 YTD |

1-Year |

Average |

Average |

|

| S&P 500 Index – Large Companies |

12.1% |

15.3% |

11.7% |

11.8% |

| S&P 400 Index – Mid-Size Companies |

5.1% |

7.9% |

8.2% |

9.8% |

| Russell 2000 Index – Small Companies |

9.1% |

12.0% |

8.7% |

9.6% |

| MSCI ACWI – Global (U.S. & Intl. Stocks) |

10.8% |

14.7% |

10.6% |

9.3% |

| MSCI EAFE Index – Developed Intl. |

3.0% |

6.4% |

6.2% |

5.6% |

| MSCI EM Index – Emerging Markets |

10.2% |

18.4% |

10.7% |

3.6% |

| Short-Term Corporate Bonds |

3.4% |

3.7% |

2.5% |

2.0% |

| Multi-Sector Bonds |

7.4% |

7.3% |

4.3% |

3.7% |

| International Government Bonds |

6.1% |

6.7% |

4.4% |

1.1% |

| Bloomberg Commodity Index |

-7.7% |

-3.1% |

-0.6% |

-6.0% |

| Dow Jones U.S. Real Estate |

-7.6% |

-6.7% |

6.4% |

8.9% |

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment, strategy, or product or any non-investment related content, made reference to directly or indirectly in this newsletter, will be suitable for your individual situation, or prove successful. This material is distributed by PDS Planning, Inc. and is for information purposes only. Although information has been obtained from and is based upon sources PDS Planning believes to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of PDS Planning and are subject to change without notice. PDS Planning assumes no liability for the interpretation or use of this report. Consultation with a qualified investment advisor is recommended prior to executing any investment strategy. No portion of this publication should be construed as legal or accounting advice. If you are a client of PDS Planning, please remember to contact PDS Planning, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives. All rights reserved.